In this illuminating interview with Seyi Abiodun, a dynamic entrepreneur and financial guru, he takes us on a journey through his personal evolution and financial insights. From humble beginnings to navigating corporate corridors, Seyi’s story is a testament to the power of resilience and learning from life’s twists and turns. With humour, honesty, and a passion for education, Seyi shares practical strategies for achieving financial freedom and making a lasting impact in our world today.

Who Is Seyi Abiodun? Walk Us Through The Journey.

Most people don’t start their lives being sure about the exact thing they want to do. They just did what their hands found to do. This is my philosophy about life. The way I like to call myself is, “I’m a doing guy, constantly doing something,” because it is in doing something that you stumble into purpose. A lot of people who are successful today, if you ask them, were unsure at some point in their lives.

For me as well, that’s how it happened, even though I read accounting, I made a detour out of accounting. I went into human resource management and business management, and I’m currently studying for a doctorate in management. Most of my work experiences revolve around management, essentially understanding how to run businesses, from the corporate level and that’s where the name “Seyideassistant” came from.

My second official job was as an Executive Assistant. Since that time, I’ve been privileged to work with business leaders, and I think that is what contributed to the body of knowledge that I have because I learnt directly from the best- CEOs, chairmen, and presidents of companies, working with them exposed me a lot. I’ve been able to learn from this in the last 14 years, before determining to stand on my own. This is what I feel that I have passion for.

Why Financial Intelligence?

First, it’s because of my personal experience. I am not disconnected from my background. I know where I’m from. When I was in school, I remember once the school fee had been paid, that is it, no luxury of pocket money. Once you get to school, you must find a way to take care of yourself. It is sad now that most of our Owambe are gated parties, where bouncers are placed at the door (lol). When we were in school, it used to be open field parties. We dressed up, showed up, ate, and even had takeaways for like 2 days after the party. Apart from that, on some Sundays, my friends and I would go to those Mega churches in town, to wash cars. From there, I started a laundry and dry-cleaning business and then a food business. My food business was roadside, we were making akara, fried yam, potato chips etc. These are all the experiences I’ve had in the past. So, bringing everything together, I see that God has taken me through all these experiences so that I can help.

Finance is a big deal. I’ve lost a lot of money. My first ever 1 million was lost to a scam investment. It took me 3 years to save the 1,000,000 naira, and I knew I could help people preserve theirs. I had this experience also, a logistics business I own ran into a lot of troubles. I had debt on my neck then that led to worry, it was difficult. Then I started reaching out to friends, one of the strategies that I found out on how to get out of debt which I also wrote in my book, is family and friends.

God put you in a family for a purpose, and you can always leverage your social capital. So, I reached out to my family and friends and started talking to them, and then I found out that the people I was talking to had more problems than I had. I don’t know if that is a Nigerian thing, the way we compete with problems. I figured that people have these challenges. What can I do? How can I start helping people with similar problems? And that was the time that loan apps also came, and they were dealing with a lot of people. 2020 was when I started this content creation around finance. I’ve seen a lot of discussion online about loan apps and gotten text messages myself.

The question now is, how can we start educating people? I probably had like 1,500 followers or so. I wasn’t expecting anything, quite honestly. If anyone had told me 3 years ago that I would have 50k followers, I would tell them that it was not possible. Till now, my goal has not still to monetize my content.

Have you been broke after you’ve started making money to the point of running into debt and how did you get out of it?

Broke is temporal, poor is a permanent type of broke. At a particular point in our lives, we would most likely be broke but the challenge is when your being broke now persists. If it becomes you are earning money, and then you’re constantly broke. That’s where the problem is. So sometimes you may be broke because you don’t have liquid cash, your cash is going into an investment. That’s another dimension of being broke. There is another dimension, where you are “broke broke”

When I moved back to Lagos, I was using my Android phone, and then I saw that a guy who was to mentor me had both an iPhone and an iPad. He introduced me to leasing, where you pay 20% and they loan you 80% with interest. That was how I started the journey into consumption debt that eventually left me broke.

I started to travel on credit (lol). I would take a six-month loan, I’ll go to Dubai, enjoy myself, then come back and start paying the loan. I’ll go to South Africa, blow the money come back and start paying the debt.

One of my most respected public figures said it better “intelligent people making unintelligent decisions.” Once my salary enters today, from 150k, Bank A takes 50k, and microfinance, 40k. At the end of the day, I’m left with 30K for the whole month, and I have transport and monthly expenses to take care of.

I’ve lived this kind of life and I can confidently say that it is not a good way to live. You’re constantly stressed, praying, and thinking about bills. Now, quite honestly, I don’t pray about money, I have better things to pray about. For instance, now I see no reason why someone should be praying for rent. God gave you a job that you should sit down and plan your rent from. Rent is not an emergency, because you had at least one year’s notice. What I did at the beginning of when I started having financial sense was to open a Fintech account, the one that allows me to lock up my savings. I have different kinds of savings, one of the savings I have is consumption savings. As of today in April, I’ve paid my rent, not to my landlord but to that account that I created. By December, when I want to pay my Landlord, I simply take the money from that account and pay my landlord.

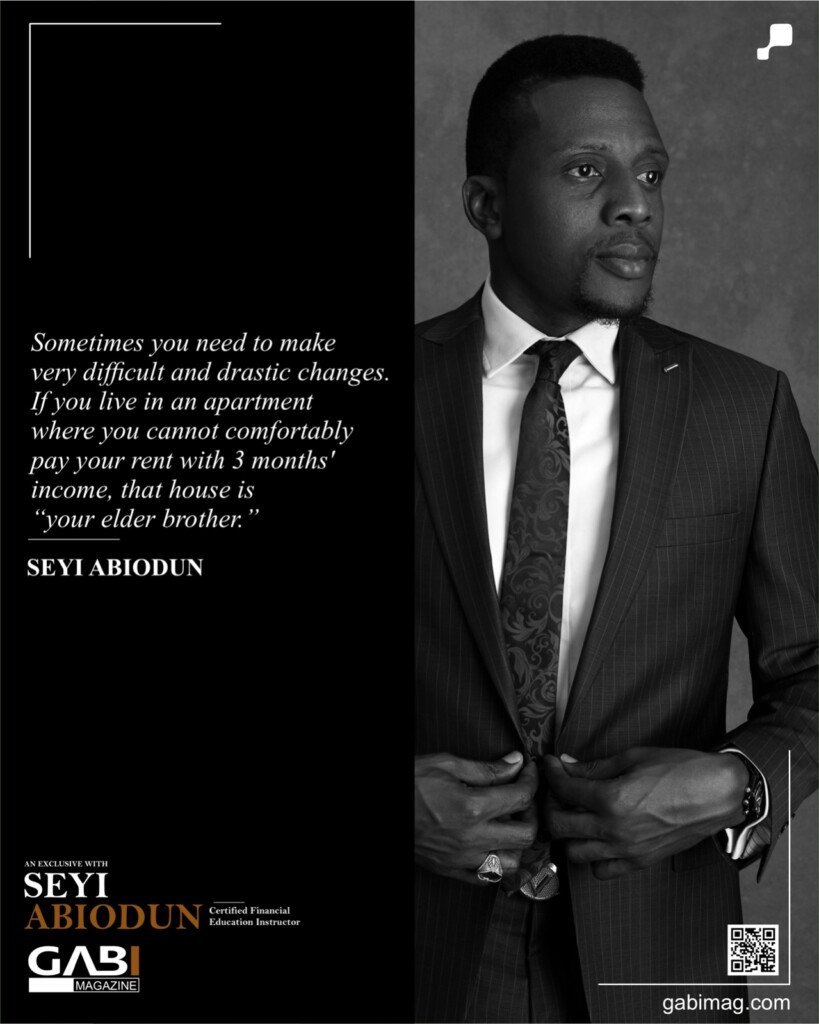

How do you come out of being broke? Learn to budget. We cannot overemphasize it. Sometimes you need to make very difficult and drastic changes. If you live in an apartment where you cannot comfortably pay your rent with 3 months’ income, that house is “your elder brother.”

For Individuals In The Career Space In Africa, What Do You Recommend For Them To Escape The Economic Uncertainties And Plan Their Finances For A Long Time?

·

The first thing to understand is the economy is divided into 3. The global economy, the national economy, and there is personal economy. A lot of times, the global and national economy is out of your sphere of control. There is nothing you and I can do about the Naira and Dollar exchange rate because we are not the government with fiscal or monetary policy responsibilities, the only one we can control is our economy.

What I advise people to do is on how to balance their finances by doing these 2 things. Number one is to find a way to increase your income. Some people do not have spending problems. What they have is an income problem.

I used to give an example of my driver, the guy earns 50K, obviously not enough. He has a wife and 3 kids, 2 in university and 1 in secondary school. He has one Jalopy car that he drives to work. On his way to work, he picks up passengers. When he gets home, he does another 2-3 hours of carrying passengers. He started saving that small money and was now able to buy a freezer to start an ice-block-making business.

A lot of people who claim to be educated are not financially intelligent. Well, we now resort to complaining. If you have a 9 to 5 and your income is not enough, especially in this economy, your 5 to 9 becomes an asset. That is the time you are not at work. You need to start thinking of how to make money, during that time, and the truth is, the opportunities are endless.

What Is Your Concept On Financial Intelligence And Financial Freedom? Is There A Point Where They Collide?

Financial intelligence is what leads to financial freedom, ultimately. If you are not financially intelligent, your financial freedom is limited. Financial freedom is the point where the return on your investment can comfortably pay your day-to-day expenses. And I would also like to say that financial freedom is very contextual and very individualistic. We are different human beings. Your idea of wealth is not my idea of wealth. One may be interested in having a company that employs 10 people. But some other people would say, I want to have a company that will employ 1,000 people. Financial freedom is going to be different. The way they define it will be different.

How Do You Track Your Financial Progress? What Are The Benchmarks To Look At?

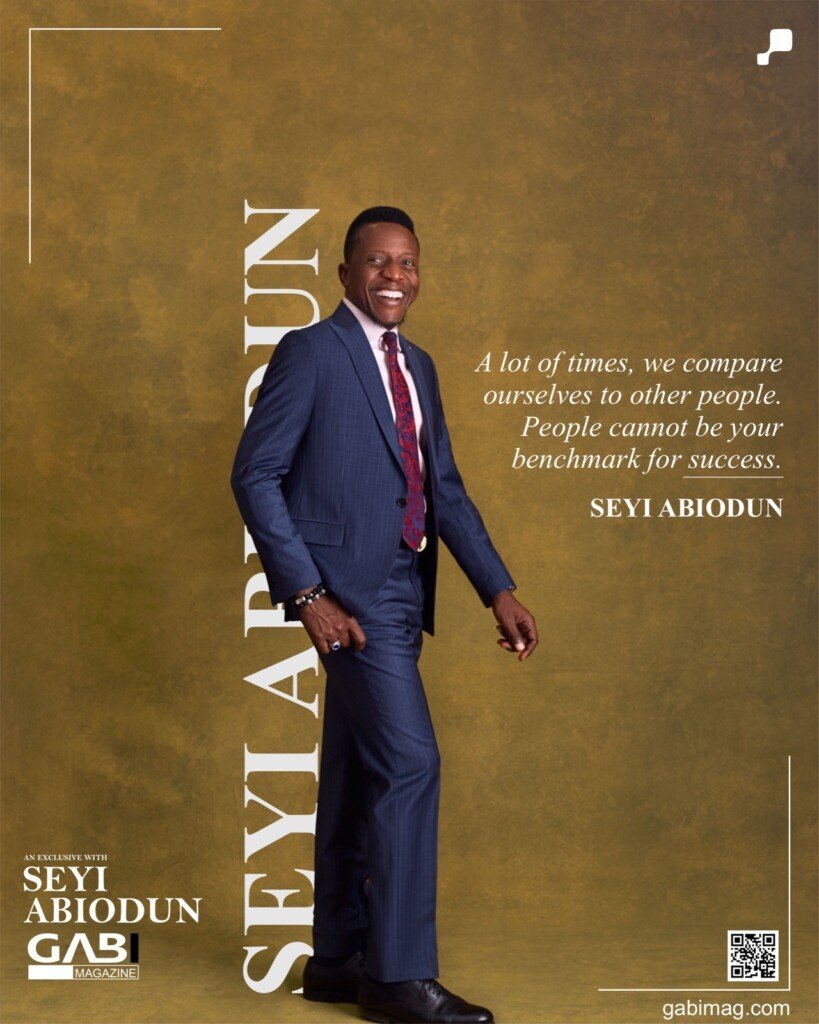

A lot of times, we compare ourselves to other people. People cannot be your benchmark for success. You know, we talk about business plans a lot, but there is something called a financial plan. A financial plan has 7 components. Everyone should have a financial plan, a document that shows you your financial roadmap. Number one of the components of a financial plan is your budget. Two are your financial goals, short-term, medium-term, and long-term financial goals. How much do you want to earn? How would you earn it? What are the things that you would do to earn it? The next component is debt management. If you have debt, what is your plan? What do you intend to do to pay off your debt? Networth is another component of your financial plan. Also, insurance.

People need to pay attention to their financial plans. Once you have a clear-cut, written-down goal, you can track your progress with it and break your goals into short medium, and long term. I’m talking about investment as well. I use that catchphrase, “gets rich slowly.” You know we are used to getting rich quickly. I am turning it around to say that we should learn to get rich slowly. Invest in all these assets. There are different kinds of assets, fixed income assets, and variable income assets, to ensure that your assets are well diversified.

When I take my classes, I talk about stocks. I remember last year; in January I bought a particular company’s stock. I bought it when it was N1.13K, today, that stock is 14/unit

Investments are also divided into 3. There is the low-risk investment, medium-risk, investments, and high-risk investments. I think that wealth building largely rests on knowledge. There are things I also don’t know fully right now. I was telling someone today that I didn’t sleep on time, I slept at 4 am because I was reading. I needed to read, I have a list of what I must complete every night before I sleep, so my sleeping time depends largely on that. If I read it quickly, fine. Discipline is the way to grow and retain wealth!

How Do You Advise To Diversify Intelligently?

If you don’t have much funds, there is a limit to your diversification. What I always advise people who are just starting is to choose 2 kinds of investment. The first one is the money market, mutual funds, which is more like a high-yield savings account.

Someone who earns NGN100,000, right after you have removed your basic expenses. Everything comes to NGN80,000 and you are only left with NGN20,000. You can use that to build a portfolio, 50% of it goes to your money market account, and then the remaining 50% goes into your stockbroking account.

A lot of mutual funds pay between 15 to 17% right now annually, and this is compounding every year. It’s a lot of money, right? I rather just put my money there than put my money in a bank account, so everyone can start from where they are. Don’t also forget that you’re keeping your eye on how to increase your income, because 100k is not enough. I’ve told some people to have an exit plan.

The plan could mean that for the next one year, you want to save. Some people may have to transition because they are in a low-paying career.

Looking At the Increase In Digital Currencies, How Should People Respond To It?

I don’t think it’s something anyone can run away from. All your assets should be divided into 3 classes, 50% into low-risk assets, 30% into medium-risk, and 20% into high-risk assets. Crypto and starting your business fall under high risk. “Don’t put over 20% of your assets into high risk. It means that if you lose your 20% in crypto, you cannot go and take 30% from another asset and invest in crypto, that would be financially unwise. If you are starting crypto, the first thing I tell people is to find someone who is good in that space. Go and learn.

Where Do You See Your Brand in The Next 10 Years?

I’ve created a bit of structure around it. It has gone beyond just trying to help people. You know I have an advisory business, an influencing business right now, and a training business right now. So I train, advise, and I also influence. Those 3 things are things that I do right now, and they are long-term for me.